Those who saw Cedric Burnside play Peppermint Bay on 8 March 2020 had a wonderful evening out. Which is just as well, as that was likely their last night out for three months. Long as these months have been, we’d do well to consider them Chapter One of The Epic of The Corona.

Tragedy and trauma there’s been aplenty, and already hints of lasting scars lead us into Chapter Two. There have been pleasant surprises, too. Who among us, for instance, could have anticipated LNP ministers, state premiers and (gasp) union leaders politely sitting down together to develop rather good policy?

But back to those lasting scars.

You can tell the heroes of the story so far aren’t going to stay friends. Their back-stories simply won’t allow it. Hostilities will surely be resumed in Chapter Two, as our heroes discover the nature and magnitude of the enduring damage and furiously produce a policy response. They’ll have to be quick, as the economic support mechanisms in place are scheduled to end in late September.

Treasurer Frydenberg tells us ‘there is no money tree’

Will we see the federal government revert to type? They are, after all, essentially suspicious of government interference with ‘the free market’, believing only the latter ensures the efficient allocation of resources. When Treasurer Frydenberg tells us ‘there is no money tree’ and Prime Minister Morrison promises the recovery will be ‘business-led’, that’s where they’re coming from. We are told Government’s role will be to provide the tax cuts and ‘flexible labour markets’ business will need to do the job. These are the ideas of classical economics. Some call it supply-side economics.

The trouble with the supply side is it wasn’t helping all that much even before the virus hit town. Gross Domestic Product (GDP) was growing at around two per cent, well down on the historical average. It would have been much lower had it not been for good iron ore prices and as much government spending as the spectre of a balanced budget would allow. That the government was already greasing the wheels of the economy is firm evidence they knew the economy was in trouble long before the word ‘Wuhan’ entered our vocabulary.

Retail and construction were already in recession, wages were flat, unemployment was rising and the Australian people were so nervous they were actually trying to save. Even the rich were pulling their heads in. Private investment had been falling since 2018.

The government plan to cut the corporate tax rate ignores the simple truth that the tax rate is not nearly as decisive a factor in investment decisions as the likelihood of an actual profit, and Australia is already a relatively low-taxing country. If foreign direct investment is not as high as it has been, it hasn’t deteriorated as badly as global foreign direct investment flows have since 2015. It is not just Australia’s economy that has been struggling to grow.

The idea of making labour markets more ‘flexible’ is fraught, too. Its defenders maintain that if employers haven’t the right to hire, fire, set wages and change rosters at will, they lose the capacity to respond to changing market conditions. This, they argue, cuts into their competitiveness at best and their very viability at worst.

Opponents point out that what employers are really proposing is to undermine the economic security workers need to plan and consume. This would bite chunks out of the 56-per-cent wedge of the economy that is consumer demand, exacerbate the economy’s fragility during downturns, and empower an already powerful minority at the expense of the vast majority.

Fully twenty-two per cent of Australia’s workforce is already casually employed. Wages have been flat for years, and the workforce’s share of national income has been falling since the eighties. Surely, weakening the hand of the already indebted worker and consumer in these straitened times would, at best, amount to scratching where it does not itch?

There is a school of economics that does not share the government’s belief in unfettered markets. It notes that we seem to have unemployment and underemployment most of the time, that things go wrong rather often, and that when they do everyone turns to government anyway. Theirs is a demand-side economics. Though such arguments don’t seem to have served the Labor Party well of late, that tide may have turned.

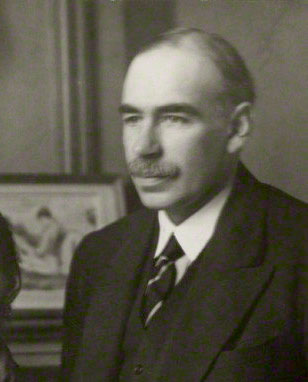

John Maynard Keynes is the fellow most associated with this line of thinking. He was watching the world sink into The Great Depression in the 1930s and wondering why things weren’t righting themselves. After all, classical economics held that if demand fell, prices and wages would fall, employers would then be motivated to buy more equipment and employ more labour, and the economy would be duly reinvigorated. That’s what business-led recoveries look like in the text-books, and the 1930s did not look like that at all.

One of the things Keynes did notice was that most prices and wages responded slowly to the obvious decline in demand – they were ‘sticky’. Economic output is made up of consumption, investment, net exports and government purchases. With all four of those falling, economic output was obviously in crisis. If prices and wages don’t fall in immediate sympathy, the crisis becomes that bit pointier, as the costs of production remain high just as effective demand deteriorates.

Keynes argued that the one determining component over which government has direct control is ’government purchases’. If wages and prices are as sticky on the way up as they are on the way down, it follows that government spending must raise economic output. This would promote employment and, thus, demand. He theorised the economy would then grow by more than the amount of government’s initial investment (this he dubbed ‘the multiplier’). All the government had to do then was manage the economy so that the implicit boom/bust cycle might be ironed out. Simple.

Sort of.

Germany and America applied Keynesian pump-priming in the thirties and forties, and, for the most part, it worked. It worked for a while when people tried it in the sixties and seventies, too. And then it stopped working.

The reason was that wages and prices are sticky for only so long. As Anwar Shaikh notes, in the Germany and America of that time, governments had the power to control wages and prices. In the 1970s, governments had no such power, and wages and prices eventually rose far enough to press profitability down and push unemployment up. So the pump-priming part of Keynes’s theory is all about economic policy in the short run. In other words, it’s about getting through crises.

Let’s have a quick look at how wages and prices have been faring in Australia.

As a proportion of GDP, wages have in fact actually gone down nearly ten per cent since the late seventies

Recent history does not favour a v-shaped recovery in employment (although it should quickly snap some of the way back as the lucky ones return to work in June and July). Australia may have dodged recessions since the Global Financial Crisis (GFC) of 2008/9, but employment here never got back to pre-crisis levels, meaning wages have hardly budged in years. As a proportion of GDP, wages have in fact actually gone down nearly ten per cent since the late seventies. In short, if there’s an argument to be made against Keynesian pump-priming, the danger of a wage break-out isn’t it.

Private debt is a far more pressing issue in Australia than the public debt we are so exhorted to fear. Compared to their counterparts in most countries, Australian consumers owe a fortune. A lot of that debt is due to the cost of housing, an asset of fragile and fluctuating value for the foreseeable future. None of this bodes well for effective demand, and the Reserve Bank has been unable to lift Australian inflation towards its two per cent target since 2013. In short, rising prices (with some exceptions, depending on trade and policy futures) present as vanishingly small a threat as rising wages. Keynesianism seems very much the way to go.

All the more so in Tasmania.

Tasmania is at several disadvantages. Historically, the state always takes longer to recover from economic shocks than its mainland counterparts. It took years after the 1918/19 flu pandemic and did so again after the 2008/9 Global Financial Crisis.

Tasmania has the oldest, least educated and most casualised work force of all the states. To make matters worse, Tasmanians work in the wrong industries. In no other state does the tourism sector absorb seventeen per cent of the workforce. Tourism contributed nearly $3 billion to the state economy last year, and no other state depends on the sector for fully ten per cent of its gross product. Tourists are going to be thin on the ground for some time.

Any denizen of the Channel or the Huon need but look at the hushed main streets of their local towns to see what that means. Even if most of these little shops, restaurants, cafés and pubs manage to open their doors again, the corona recession and its legacy suggests some might be gone by Christmas.

Let’s look at the cafés. Large ones typically make enough profit to endure a three-month suspension of business. Small ones, of which rural Tasmania has many, struggle to make a profit of five per cent of gross sales. Even if the proprietor survives the public health emergency, effective demand will not fully recover while the locals nervously tighten their purse-strings and tourists are locked out. So if a business-led recovery it is to be, it’s hard to see it kicking off unaided here.

Indeed, if we factor in the decimated retail and arts/recreation sectors, we’re looking at eight per cent of Tasmanians losing their jobs, and an unemployment rate of twelve per cent. If the China thing deteriorates, agriculture here begins to suffer because Tasmania produces just the sorts of luxuries and delicacies China thinks it can go without for a while. The university would, of course, descend into a deep dark pit, losing around 20% of its annual revenues. To make matters worse, Tasmania depends disproportionately on its disproportionate GST allocation, and the GST take for the second half of this financial year will not make for pleasant reading.

If JobKeeper closes and JobSeeker is cut back in late September, and if loan deferrals and rent relief expire at the same time, Australia will face homeless families, distressed selling, plunging house prices, and collapsing demand before Christmas. That’s how urgent the situation is.

The government’s public works budget should be expanded, with ‘shovel-readiness’ a decisive criterion. Money has never been cheaper and the Reserve Bank could just buy more government bonds than it’s buying already. An added bonus is that this guaranteed demand for bonds should help keep interest rates low. Australian household debt is such that low interest rates will be essential for years to come.

Not all hope is lost, of course. Among Tasmania’s many germane blessings are:

- a climate that everyone has begun to realise is better suited to the decades to come;

- a relatively large public-sector that has continued to pay its workforce;

- an environment likely to attract many professionals seeking to take advantage of the technically feasible and recently invigorated tele-commuting ethos;

- the charms to attract thousands of well-heeled Australian boomers looking to retire to milder climes;

- the sexiest museum in the country;

- a premier who went farther than most in budgeting for what’s coming;

- the battery-of-the-nation proposal;

- a university desperate for students just as the health and engineering sectors approach an exodus of retirees,

- loads of primary produce that would benefit from more local processing capacity, and

- already identified infrastructure projects that are close enough to shovel-ready to make a difference when it’s needed. Social housing, urban-fringe bushfire buffer zones, and a still chronically underfunded health sector come to mind.

As for the touted renovation-led recovery, well, it’ll make renovations more expensive. The banks should benefit, along with some tradespeople and a small posse of daring or wealthy homeowners. The policy’s political virtues are moot and it is hardly optimal economics.

Construction promotes ancillary businesses, implying a promising multiplier effect.

At least Premier Gutwein has put $100 million aside for social housing. The attendant first-home builders’ grant ($20,000 per owner-occupier, on top of the $25,000 the federal government is currently offering) has the virtues of adding much-needed housing stock and greasing the state’s economic wheels for up to two crucial years. Construction promotes ancillary businesses, implying a promising multiplier effect. It might even attract some enterprising young folk to the state. But it does have a flaw to which all such incentives are prey. It risks inflating the cost of the private renovations, and if it does that, the social housing program could suffer, too. Not all prices are sticky.

The Morrison Government has shown us that it’s capable of consultation across venerable battle lines when it perceives a crisis. It has even been prepared to embrace the alien precepts of Keynesian economics. Good on it. It may not feel like it, but most of us are reaping the benefits. That’s how bad this thing could have been.

The thing is to realise how bad things can still be, that the federal government will be running an economy in crisis for at least the rest of its term. Chapter Three of the Epic Of The Corona won’t be written until July. There had better be more to it than corporate tax cuts and ‘flexible labour markets’, or it’ll make for awful reading.

{kind=link}